We've got you covered

We are here to guide you in making tough decisions with your hard earned money. Drop us your details and we will reach you for a free one on one discussion with our experts.

or

Call us on: +917410000494

While we were discussing Return on Equity, and the DuPont analysis, we touched on the topic of financial leaning. Leverage (debt) can be a double-edged sword.

If they see a situation in which they can use the debt funds to generate a higher return than the interest payments, well managed companies will seek out debt. Remember that judicious debt use can increase the return on equity.

If a company has too much debt, the interest that is paid on the debt can eat into shareholders' profit share. There is no clear line between good and bad debt. The company's overall debt load is what we use to calculate the leverage ratio. It also helps us better understand its financial leverage.

The following ratios will be examined:

We have used Amara Raja Batteries Limited, (ARBL), as an example. However, to understand leverage ratios we will examine a company with a large amount of debt on its balance sheets. Jain Irrigation Systems Limited, (JISL) has been my choice. I encourage you to calculate the ratios for any company that interests you.

Ratio of interest coverage:The interest coverage ratio, also known as the debt service ratio, or the debt coverage ratio, is also known. This ratio shows how much the company is making relative to its interest burden. This ratio allows us to determine how easy a company can pay its interest. If the interest burden is Rs.100 and the income is Rs.400, we can see that the company has enough funds to pay its debts. A low interest coverage ratio can mean that the company has a higher debt burden, and there is a greater chance of default or bankruptcy.

Here's how to calculate the interest coverage ratio[Earnings Before Interest and Tax / Interest Payment][

The EBIT (earnings before interest and tax) is:

EBITDA - Depreciation & Amortization

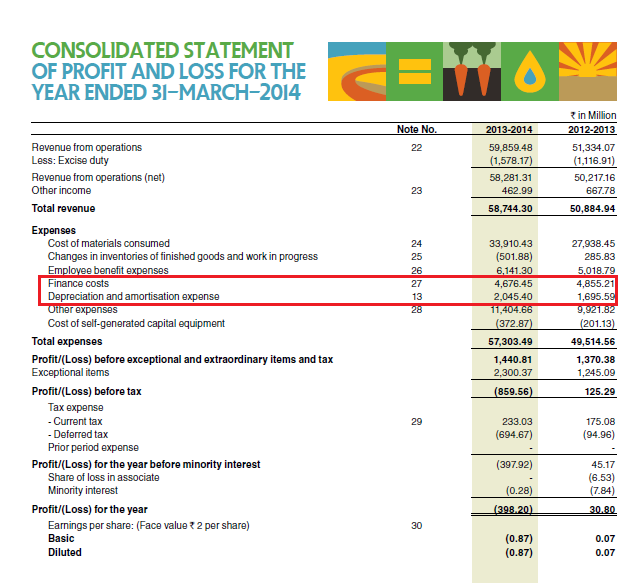

Let's apply this ratio to Jain Irrigation Limited. Here's a snapshot of Jain Irrigation’s P&L Statement for FY 14.The Finance cost has been marked as red.

EBITDA is [Revenue - Expenses].

We subtract the Finance cost (Rs.467.64Crs), and the Depreciation, Amortization cost(Rs.204.54) from total expenses of Rs.5730.34 Cros.

EBITDA = Rs.5828.13- 5058.15 Crs

EBITDA = Rs. 769.98 Crs

EBIT = EBITDA = [Depreciation and Amortization]

= Rs.769.98- 204.54

Rs. = Rs.

We know that Finance Cost is Rs.467.64

Therefore, interest coverage is:

= 565.44/ 467.64

= 1.209x

The number 1.209x is a multiple. Therefore, 1.209x should not be read as 1.209 "times".

Jain Irrigation Limited generates an EBIT of 1.209x for every Rupee due in interest payments. This is a coverage ratio of 1.209x.

Ratio Debt to Equity: This ratio is quite simple. The Balance Sheet contains both variables needed for this calculation. It is used to measure the ratio of total debt capital to total equity capital. This ratio is equal to the equity capital and debt. A value of 1 indicates that there is no debt. A higher ratio of equity to debt (more than 1) means that there is more leverage. Therefore, it is important to be cautious. A lower ratio of debt to equity (less than 1) indicates a larger equity base relative to the debt.

This formula calculates the debt to equity ratio:

[Total Debt/Total equity]

Note that the total debt includes both short-term and long-term debt.

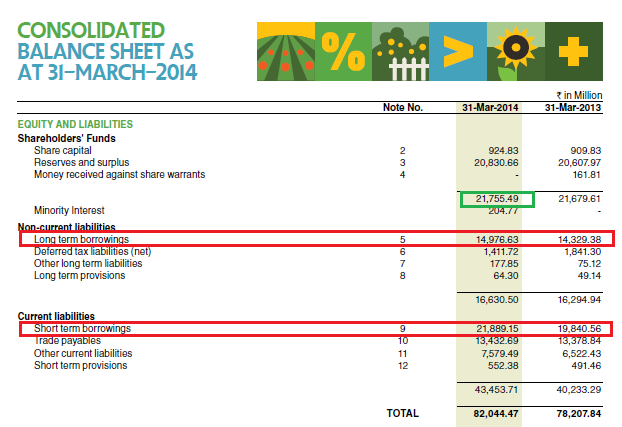

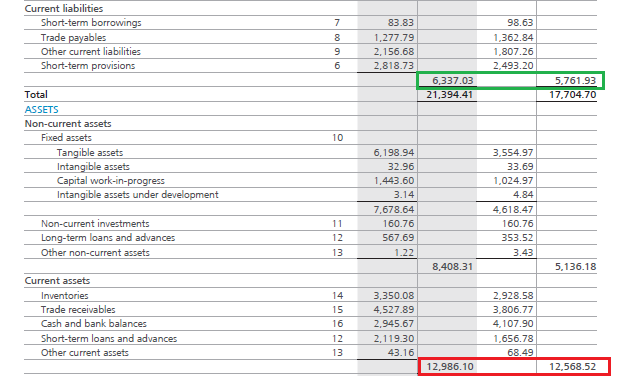

Here's JSIL's Balance sheet. I have highlighted total equity and long-term debt.

Total debt = Long-term borrowings + short term borrowings

= 1497.663 + 218.915

= Rs.3686.578Crs

Total Equity: Rs.2175.549 Crores

The Debt-to-Equity ratio will thus be calculated as follows:

= 3686.578/ 2175.549

= 1.69

Ratio of Debt to Asset:

This ratio allows us to understand the company's asset financing patterns. This ratio shows us how much of the company's total assets can be financed by debt capital.

This formula will calculate the same:

Total Debt/Total Assets

We know that the total debt of JSIL is Rs.3686.578Crs.

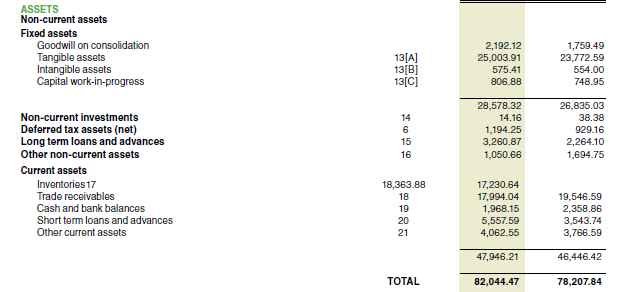

We know that the assets total amount to Rs.8204.44747 Crs from the Balance Sheet.

The Debt-to-Avail ratio is therefore:

=3686.578/8204.44

= 0.449, or 45%

About 45% of JSIL's assets are financed via debt capital or creditors. 55% of JSIL's assets are financed by their owners. As you can see, the higher the percentage, the greater the risk and leverage for the investor.

Financial Leverage Ratio

In the previous chapter, we briefly discussed the financial leverage ratio. We also talked about Return on Equity. We can see how much equity is supporting assets from the financial leverage ratio.

This formula calculates the Financial Leverage Ratio.

Average Total Asset/Average Total Equity

JSIL's FY14 financial balance sheet shows that the average total assets are Rs.8012.615. The average equity is Rs.2171.755. The financial leverage ratio, or simply the ratio of leverage, is:

8012.615/ 2171.755

= 3.68

JSIL supports Rs.3.68 unit assets per equity unit. Remember that the higher the number, the greater the company's leverage.

Operating Ratios, also known as 'Activity rates' or 'Management ratios, indicate the efficiency of a company's operational activities. The operating ratios can also reveal the efficiency of the management. These ratios are known as the Asset Management Ratios. They indicate how efficiently the company's assets are used.

These are some of the most popular Operating Ratios:

These ratios combine data from the Balance sheet and P&L statements. These ratios will be explained by Amara Raja Batteries Limited.

One must compare operating ratios between companies with similar businesses to get an accurate picture of the company's performance.

Fixed Assets Turnover

This ratio shows how much revenue is generated compared to the amount of fixed assets it has invested. This ratio shows how efficient a company's plant and equipment is used. The property, equipment and plant are considered fixed assets. A higher ratio means that the company manages its fixed assets more efficiently and effectively.

Fixed Assets Turnover = Operating Incomes / Total Average Asset

When calculating fixed assets turnover, assets should be net of accumulated deduction. This is the net block of the company. This should include capital work in progress. We also take the average assets, as discussed in the previous chapter.

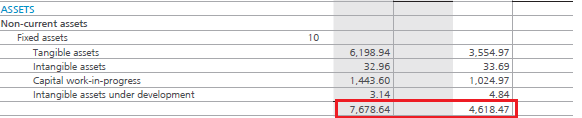

ARBL's FY14 Balance sheet:

= (767.864 + 461.477)/2

= Rs.614.855 Crs

Operating revenue for FY14 was Rs.3436.7 Crores.

Hence, the Fixed Asset Turnover ratio(FATR) of:

= 3436.7 / 61.85

=5.59

When evaluating this ratio, keep in mind where the company is at. A company that is well-established may not use its cash to purchase fixed assets. For a growing company however, it may invest in fixed assets. The fixed asset value could increase each year. This is also true for ARBL. For FY13, Fixed assets value was Rs.461.8 Crores. For FY14, fixed asset value was Rs.767.8 Crores.

This ratio is used by capital-intensive industries to evaluate how efficiently the fixed assets are being used.

Turnover of working capital

The firm's working capital is the amount of capital it needs to operate its day-to-day operations. A certain type of asset is required to run day-to-day operations. These assets include cash, inventories, receivables and cash. These are your current assets. A well-managed company finances its current assets using current liabilities. The difference between current assets and current liability is Working Capital.

Working Capital = Current Assets - Current Liabilities

If the company's working capital is positive, it means that they have sufficient capital.working capital surplusIt is able to manage its day-to-day operations easily. If the company's working capital is negative it means that the company does not have enough money.working capital deficit. If the company has a deficit in working capital, they will usually seek a working capital loan from the bank.

Corporate Finance is full of the concept of "Working Capital Management". This includes inventory management, cash management and debtor's management. The chief financial officer (CFO) of the company strives to efficiently manage the company's working capital. We won't get into the details as it will distract from the main topic.

Also known as Net sales to working capital, the working capital turnover ratio (or net sales to working capital) is also known. The company's working capital turnover is the amount of revenue it generates for each unit of working capital. If the ratio is 4, it means that the company generates Rs.4 per Rs.1 in working capital. It is obvious that a higher number indicates a better ratio. To get a better understanding of the company's performance, all ratios must be compared to its peers/competitors within the same industry.

Here's how to calculate theWorking capital turnover work Capital Turnover = [Revenue/Average Working Capital]

Let's do the same with Amara Raja Batteries Limited. First, calculate the FY13 and FY14 working capital and then calculate the average. Here's a snapshot of ARBL’s Balance sheet. I have highlighted current assets (red), and current liabilities (green), for each year.

Here is how to calculate the average working capital over the two financial years:

| Current Assets for the FY13 | Rs.1256.85 |

| Current Liabilities for the FY13 | Rs.576.19 |

| Working Capital for the FY13 | Rs.680.66 |

| Current Asset for the FY14 | Rs.1298.61 |

| Current Liability for the FY14 | Rs.633.70 |

| Working Capital for the FY14 | Rs.664.91 |

| Average Working Capital | Rs.672.78 |

ARBL's revenue from operations is estimated at Rs.3437 Crs. The working capital turnover (WCT) ratio is:

= 3437 / 662.78

=5.11 Times

This number shows that every Rs.1 of working capital generates Rs.5.11 revenue. The higher the ratio of working capital turnover, the better. This indicates that the company generates more sales than it spends on funding.

Turnover of Total Assets

This ratio is very straightforward. This ratio indicates the company's ability to generate revenue with the given assets. This includes both current and fixed assets. The company's total asset turnover ratio is higher than its historical data or competitor data, which means it is effectively using its assets to generate more sales.

Total Asset Turnover =

Operating Income divided by Average Total Assets

ARBL's average total assets is as follows -

Total Assets in FY 13: Rs.1770.5 Crs, and Total Assets in FY 14: 2139.4 Cros. The average assets would then be Rs. 1954.95 Crs.

Operating revenue for FY 14 is Rs. 3437 Crs. 3437 Crs.

= 3437/54.95

= 1.75 Times

Inventory Turnover Ratio

Inventory is the inventory that a company keeps in its showroom or store. Its purpose is to sell the finished goods to potential clients. The company would normally keep the finished goods in its store, but also have some units in its warehouse.

A company selling popular products will have its inventory cleared quickly. The company must replenish the inventory every time. This is also called "Inventory turnover".

Consider a bakery that sells hot bread. The baker will know how many breads he can sell if the bakery is well-known. He could sell 200 pounds of bread per day, for example. He would need to keep 200 pounds of bread in stock every day. In this instance, the rate of replenishment and inventory turnover are very high.

However, this may not apply to every business. Consider a car manufacturer, for example. Selling cars isn't as simple as selling bread. A manufacturer may need to wait a while before selling 50 cars. To sell 50 cars (his inventory), he would need to wait 3 months. He will turn over his inventory every 3 months. In other words, he flips his inventory four times a year.

If the product is very popular, inventory turnover will be high. This is what the 'Inventory turnover ratio' shows.

This formula calculates the ratio:

Inventory Turnover = Cost Of Goods Sold divided by Average Inventory

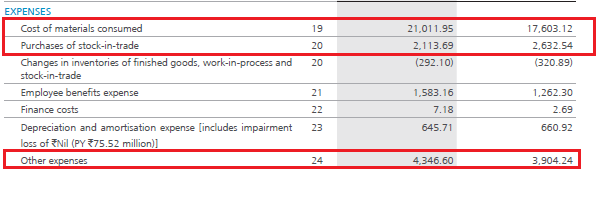

The cost of making finished goods is called the cost of goods sold. This information can be found in the P&L Statement. Let's do this for ARBL.

Here is a sample of what I found to be the most relevant:

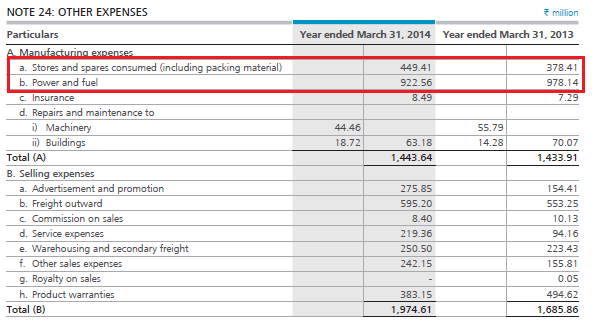

The cost of material consumed is Rs.2101.19 Cros, and stock-in trade is Rs.211.36 Cros. These line items directly relate to the cost of goods purchased. To identify costs related to the price of goods sold, I will also inspect 'Other expenses'. This extract from Note 24 explains 'Other expenses'.

Two expenses directly relate to manufacturing: The cost of stores & spares is Rs.44.94 Crs, and the cost of power & fuel is Rs.92.25Crs.

Therefore, the Cost of Goods Sold = Cost of materials used + Purchase of stockin trade + Stores and spares consumed + Fuel & Power= 2101.19 + 209.36 + 44.94 + 92.25.

COGS = Rs.2449.74 Crs

This will take care of the numerator. We simply take the FY13 and FY14 average inventories for the denominator. The balance sheet shows that inventory for FY13 was Rs.292.85 crores, and inventory for FY14 was Rs.335.00 crores. This average comes out to Rs.313.92 Cros

The inventory turnover ratio is:

= 2449.74/ 313.92

= 7.8 Times

8.0 Times per year

Amara Raja Batteries Limited rotates its inventory eight times a year, or once every 1.5 months. It is important to note that to truly understand the quality of this number, it should be compared with those of its competitors.

Stock Number of Days

The Inventory turnover ratio measures how often a company'replenishes their inventory'. However, the Inventory number in Days gives an indication of how long it takes for inventory to be converted into cash. The shorter the inventory number of days is, the better. If the inventory number is short, it means that products of the company are moving quickly. This formula calculates the inventory number of days.

Inventory Number of Days =365 / Inventory Turnover

The inventory number of days is often calculated on a yearly basis. In the above formula, 365 is the number of days in an year.

This is how to calculate ARBL

= 365 / 7.8

= 46.79 Days

47.0 Days

ARBL takes approximately 47 days to convert inventory into cash. To get an idea of the company's product movement, it is important to compare the inventory number of companies with theirs.

Here's something to think about: What do you think about this situation?

The company's inventory management looks great. High inventory turnover means that the company replenishes its inventory quickly. This is an excellent sign. A low inventory count indicates that the company can quickly convert its goods into cash. This is another sign of good inventory management.

What if the company produces a lot of product but has low production? In this scenario, inventory turnover and inventory days are high. A low production capacity can cause concern as it raises questions about the company’s production.

If any of these points is true, it is a red flag and investing in the company is not advisable. The annual report should be read from beginning to end by the fundamental analyst, including the management discussion and analysis reports.

This means that if you notice impressive inventory numbers, double-check the production details.

Ratio of Accounts Receivable to Turnover

Understanding the inventory turnover ratio will make it easy to understand the receivable turn ratio. The receivable turn ratio shows how often the company receives money/cash over a period from customers and debtors. A high number means that cash is collected more often.

This formula will calculate the same:

Ratio of Accounts Receivables = Revenue / Average Receivables

We know this from the balance sheet.

Trade Receivables for FY13: Rs.380.67 Crs

For FY14, Trade Receivables: Rs. 452.78 Crs

Average Receiveable for FY13: Rs.416.72

Operating Revenue for FY14: Rs.3437 Crore

The Receivable Turnover Ratio therefore is:

= 3437 / 416.72

8.24 times per year

8.0

ARBL receives cash approximately 8.24 times per year, or once a month and a quarter.

Days Sales Outstanding (DSO),/ Average Collection Period/Day Sales in Receivables

The days sales outstanding ratio shows the average cash collection time, i.e. the time between collection and billing. This calculation shows how efficient the company's collection department is. The cash can be used faster if it is collected quickly from creditors. Here's how to calculate the same:

Days Sales Outstanding is equals to 365 Receivable Turnover Ratio (RTR)

This is how to solve ARBL.

= 365 / 8.24

44.29 Days

ARBL can collect the money within 45 days of the invoice being raised.

The firm's credit policy is indicated by the Receivables Turnover as well as the DSO. An efficient company should find the right balance between its credit policy and the credit it extends customers.