We've got you covered

We are here to guide you in making tough decisions with your hard earned money. Drop us your details and we will reach you for a free one on one discussion with our experts.

or

Call us on: +917410000494

You should not be deceived by the 'Bear' symbol in the "Bear Call Ladder". This is not a bearish strategy. Bear Call Ladder can be interpreted as an improvisation of the Call ratio back spread. This clearly indicates that you should only implement this strategy if you are bullish on the stock/index.

A Bear Call Ladder's cost to purchase call options can be financed by selling an "in the money" call option. The Bear Call Ladder can also be set up for net credit, which is where the cash flow from the call ratio back spread is more than the cost of purchasing call options. Both strategies have similar payoff structures, but they differ in terms of risk.

The Bear Call Ladder, a 3-leg option strategy that is usually set up for "net credit", involves -

This is the classic Bear Call Ladder setup. It's executed in a 1:1 ratio. Bear Call Ladder must be executed in a 1:1:1 ratio. This means that for every 1 ITM call option sold, 1 ATM or 1 OTM call option must be purchased. You can also combine 2:2:2 and 3:3:3 (and so on)

Let's say Nifty Spot is at 7777 and you expect Nifty will reach 8100 before expiry. This is clearly a bullish outlook for the market. The Bear Call Ladder can be implemented here

You should ensure that -

This is how the trade setup looks.

The bear call ladder can be executed with these trades. Let's see what happens to the cash flow at different levels of expiry.

We need to assess the strategy payoff at different levels of expiry, as the strategy payoff can be quite flexible.

Scenario 1: Market expires at 7600 (below lower strike price).

The intrinsic value of a call options (upon expiry), is known to be -

Max [Spot-Strike, 0]

The 7600 would have an intrinsic worth of

Max [7600-7600, 0]

= 0

We retain the premium we received for this option (Rs.247/-) because we have sold it.

Similarly,the intrinsic value will be zero of 7900 CE and &800 CE,

therefore the premium paid will be lost i.e Rs. 70 and Rs.117 respectively

Net cash flow would Premium received - Premium paid

= 247 - 112 - 70

=60

Scenario 2: Market closes at 7660 (lower strike and net premium received).

The 7600 CE would have an intrinsic worth of -

Max [Spot-Strike, 0]

The 7600 would have an intrinsic worth of

Max [7660-77600, 0]

60

We will lose 60 CE from 247 because the 7600 CE is so short. However, we retain the balance

= 247 - 60%

= 187

We would lose the premium we paid, 117 and 70 respectively.

The strategy's total payoff would be -

= 187 - 112 - 70

= 0

The strategy would therefore not make or lose money at 7660. This is a lower breakeven point.

Scenario 3 - At 7700,the market expires(in between 7600 and 7800 i.e breakeven point & middle strike).

The intrinsic value for 7600 CE would be:

Max [Spot-Strike, 0]

= [7700-7600, 0]

100

We have now sold this option for 247. The net payoff from the option would then be

247 - 100

= 147

We have also purchased 7800 CE and7900 CE. Both of these options would be worthless and we would lose the premium we paid.

The strategy's net payoff would be -

147 - 112 - 70

=- 40

Scenario 4: Market expires at 7800 (at middle strike price).

This is where tragedy strikes!

We would lose the intrinsic value of Rs.200 if we had written the 7600 CE option at a premium Rs.247.

On the 7600 CE we lose 200 but retain -

247 - 209

= 47/-

Both 7800 CE as well as 7900 CE would be worthless. Therefore, the premium we paid, i.e. 117 and 70, goes to waste. Our total payoff would therefore be -

47 - 117-70

=-140

Scenario 5: Market closes at 7900 (at a higher strike price).

Attention again! Tragedia strikes again

The 7600 CE would have a value intrinsically 300. Given that we have written this option at a premium Rs.247 we are likely to lose all of the premium value and more.

Therefore, on the 7600 CE we lose -

247 - 399

= -53

The intrinsic value of both 7800 CE and Rs.117 would be 100. This would make the option a pay-off of -

100 - 112

= - 17

The premium of 70 dollars would be wasted as 7900 CE would soon expire. The last strategy payoff would be:

-53 - 17-70

=-140

Note that the loss at 7800 and 7900 are the same.

Scenario 6 - At 8040 the Market expires(sum of (long strike - short strike- net premium))

The bear call ladder, similar to the call ratio back spread has two breakeven points. These are the upper and lower breakeven. The lower breakeven was evaluated earlier in Scenario 2. This is the upper breakeven point. The upper breakeven point is -

(7900 + 7800), - 7600, - 60

= 15700 - 7600- 60

= 8100 - 60%

= 8040

Note that 7900 and 7800 represent strikes we have in excess, while 7600 represents the strike we have short. 60 is the net credit.

All the call options at 8040 would have an intrinsic worth -

7600 CE would have an intrinsic worth of 8040 -7600 = 440. Since we are short at 247, we stand for 247 -440 =-193.

7800 CE would have an intrinsic worth of 8040 - 7800 = 244. Since we are long on this at the 117, we make 240-117 =+123

7900 CE would have an intrinsic worth of 8040 – 7900 = 140. Since we are long on this at 70 we make 140 – 70 =+70

The Bear Call Ladder's total payoff would therefore be -

-193 + 12 + 70

=0

The strategy would therefore not make or lose money at 8040. This is considered an (upper) breakeven point.

Note that the strategy lost 7800 to 7900 and broke even at 8040. This should give you an idea of how profitable the strategy could be beyond 8040. Let's see if we can prove this by looking at another scenario.

Scenario 7: Market closes at 8300

All call options at 8300 would have an intrinsic worth.

7600 CE would have an intrinsic worth of 8300 -7600 = 700. Since we lack this at 247 we stand to lose 247-700 =-453

7800 CE would have an intrinsic worth of 8300 -7800 = 500. Since we are long on this at the 117, we make 500 =+383

7900 CE would have an intrinsic worth of 8300 – 7900 = 400. Since we are long on this at 70%, we make 400 – 70 =+330

The Bear Call Ladder's total payoff would therefore be -

-453 + 383 +330

=260

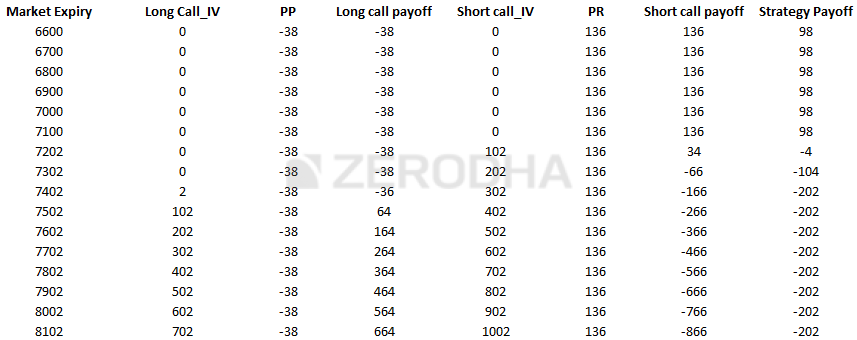

As you can see, the greater the market moves, the greater the potential profit. Below is a table showing the potential payoffs for different levels.

Notice that you can make a small gain of 60 points if the market falls below your target, but not if the market rises.

We can draw few conclusions based on the scenarios discussed above.

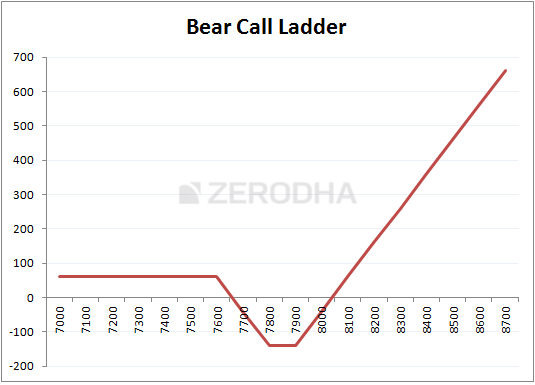

This graph highlights these key points.

The strategy loses between 7660-8040 but makes huge profits if the market goes above 8040. You still make a small profit even if the market falls. If the market doesn't move, you will be severely hurt. This is why I recommend that you only implement the Bear Call Ladder strategy when you are certain that the market will move in any direction.

Based on my experience, this strategy works best when it is executed with stocks rather than indexes.

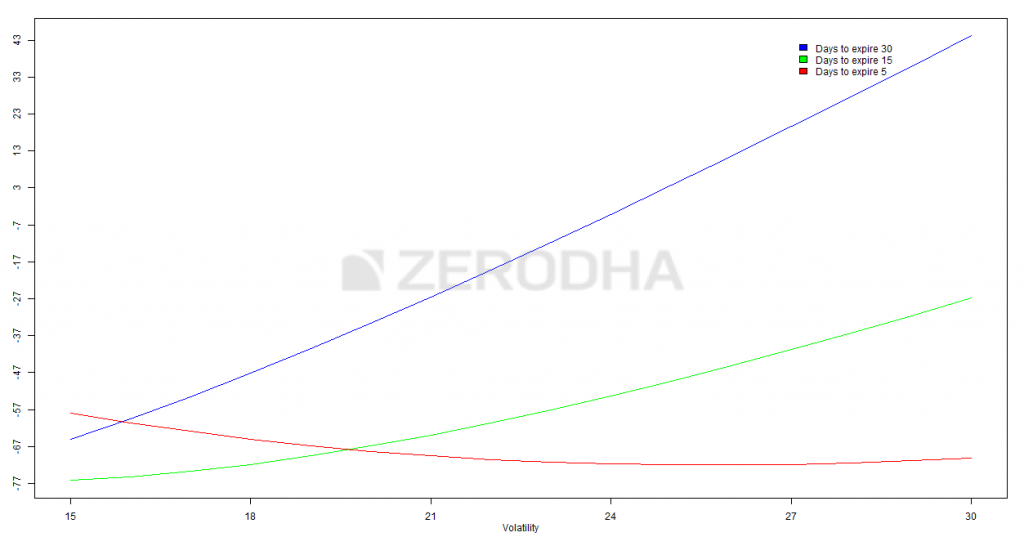

This strategy has a very similar effect to Call Ratio Back spread. The volatility bit is also affected by Greeks. For your convenience, I have reproduced the discussion about volatility that we had in the preceding chapter.

Three colored lines represent the change in "net premium", aka strategy payoff, versus volatility. These lines allow us to see the impact of volatility increase on strategy payoff while keeping time to expiry in perspective.