We've got you covered

We are here to guide you in making tough decisions with your hard earned money. Drop us your details and we will reach you for a free one on one discussion with our experts.

or

Call us on: +917410000494

At this stage, we make a critical assumption. We will assume that you are familiar with the F&o Contract.

The role of technical analysis is crucial in the setting up currency trades. We assume that you are familiar with this aspect. You can also find them here.

These topics are important and I recommend that you review these modules before you continue. A large part of the currency and commodities markets is a Futures market. Therefore, it is important to have a working knowledge about these derivative instruments.

Assuming you are familiar with these concepts, let's begin by cutting and dicing USD INR futures contracts. We can gain insight into trade logistics by looking at the contract specification for USD INR futures.

These are the key features of the USD/INR pair.

| Particular | More Details | Remark |

|---|---|---|

| Lot Size | $1,000 | Inequity derivatives: The lot is the number of shares. But here it's the dollar amount |

| The Basis | Rate of Indian Rupee to 1 USD | |

| Tick Size | 0.25 Pounds or INR 0.0025 in Rupee terms | |

| Trading hours | Monday through Friday, 9:00 AM to 5:00PM | |

| Expiry Cycle | Contracts up to 12 months | Equity derivatives can expire up to 3 months. |

| Last trading day | Contracts can be traded until 12:30 PM on the 2nd day before the end of work. | Equity derivatives can continue trading until 3:30 PM on the expiry date. |

| Final Settlement day | Last day of the month | |

| Margin | SPAN + Exposure | SAPN typically is approximately 1.5% and exposure around 1%. The overall margin requirement is therefore approximately 2.5%. |

| Settlement price | The day of Final Settlement, the RBI Reference Rate | Spot closing price |

Let's look at an example to give you an idea of how it works.

This is a 15-minute chart for the USD INR pair. You can use this to initiate a short trading with the Marubuzo as the stoploss.

Please note that I am not trying to justify trades here. My objective is to show how the USDINR contract works.

Below are the details for trade.

Date: 1 July 2016

Short Position

Entry - 67.6900

SL - 67.7500

Shortening the number of lots - 10

1 lot USD INR = $ 1000

1. Lot size = Price

=1000 * 67.7000

=67,700

This calculator will calculate the margin needed for this; here's a snapshot.

As you see, the margin needed to open a new USD INR position is approximately Rs.1,524/–. For a contract with USD 67700, this works out to be -.

1525/67700

2.251%

This would make about 1.5% the SAPN margin requirement. It is the minimum margin required per exchange. The rest would be exposure margin.

The idea is to reduce the number of lots by 10 so that there is only -.

10 * 1525

= 15,250/=

Remember that you must allocate anywhere from 15% to 66% of the contract's total value for margins when trading equity futures. This will vary from stock to stock. The margin charge in currencies is much lower than for equities. This should give an idea of the leveraged nature of currency trading.

However, currency trades within a narrow range when compared to equities. This results in higher leverage.

You can see that the currency futures are quoted up to the 4 decimal numbers. This is because 0.0025, when it comes currency futures is considered large, is very small.

The reference rate is stated by the RBI at the 4 th decimal. A small difference in the 4 th decimal could result in a significant decrease in foreign reserves. It is common practice worldwide to quote the currency to the 4 thdecimal. In USD INR's case, this is 0.0025. This is known as the tick size, or in currency parlance, a "pip". Pip/tick refers to the minimum number of points a currency can move.

According to the USD INR, the currency moved by one pip when it moved from 67.900000 to 67.9025.

What would be the average amount of money you could make per pip for USD INR pairs? This shouldn't be hard to do.

Lot Size * pip

= 1000 * 0.0025

= 2.5

This is to say that for every tick movement or pip, you earn Rs.2.5/-

Here's how the Marubuzo performed in the short trade.

The currency pair fell to 67.6000 after initiating the short. He is the amount I would make if I close this position.

Entry = 67.6900

CMP = 67.6000

Total number of points = 66.7900 - 66.76000 = 0.0900

Short Position

This can be tricky so pay attention. As you can see, a pip is the minimum amount of points a currency can move. We divide the total points moved by 0.09paise to find the number of pips.

Number of pips = 0.0990/0.0025

= 36

You can see that the trade captured 36 pip. Let us now calculate how much one would make.

Size of lot * Number of lots * Number of pips * Tick size

We are awareNumber of ticks * number of pipsIt is as good as theTotal number of pointsThis trade is a trap. We can therefore restate the formula.

Lot Size * Total number of points

= 1000 * 10 * 0.09900

=900

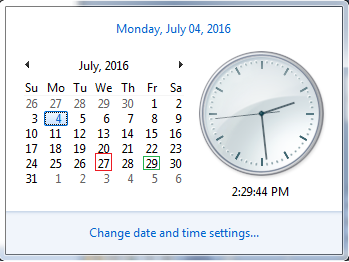

This is an intraday trade. What if you wanted to keep this trade open until expiry? We can still carry it forward, provided we meet the necessary margin requirements. The July contract will remain in series for 2 days after the end of each month.

Here's the calendar

The 29th of July is the last day of the month. This means that 27 th July will mark the end of the series. You can actually keep the contract until 12:30 PM on 27 th July.

You can always check the contract to find the exact expiry date.

Another question is: at what price settlement will occur?

Settlement will take place at the RBI reference rate for 27 July. It is important to remember that the P&L will not be settled in rupees.

For example, let's say I held this position until 12:30 PM on 27 July, and then let it expire. Let us assume that the price is 67.4000. I'd then be able make -

1000 * 0.29 * 10.

=2900/-1

This money will be credited on my trading account on the 28 th July 2016. As long as the contract is held, your position will not be marked to market (M2M). It is the same as for equity futures.

This example should hopefully give you an idea of the logistics involved in currency futures.

Let's quickly go over the USDINR options contract.

Let's take a look at the structure of the USDINR option contracts. It may interest you to know that the option contract only applies to the USD INR currency pair. We may soon see option contracts for other currency pairs. Although most of the parameters are the same as the futures contract they have few unique features.

Expiry option- European

Premium- INR quoted

Contract cycleFuture contracts can be purchased for 12 months ahead, but options contracts are only available for 3 months. This is similar to equity derivatives. Since we are currently in July, contracts can be purchased for July, August and September.

Strikes available- 12 in the Money, 12 out of the Money and 1 near the money options. This gives you roughly 25 options to choose from. You can add more options depending on the market. Strikes can be taken at 0.25 paisa intervals.

Settlement- Settlement in INR based upon the settlement price (RBI Reference Rate on Expiry Date).

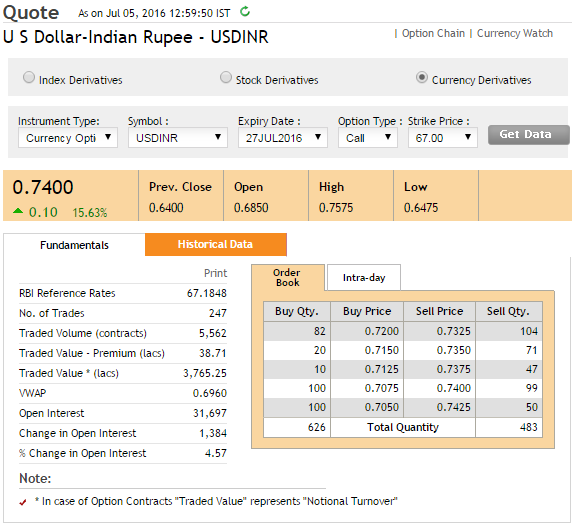

Let's take a look at USD INR option contracts and work out the logistics. Take a look at this image.

We know these things from the option quote

Option type - Call option

Strike - 67.0000

Spot price (see RBI Reference Rate)-67.1848

Expiry Date: 27 th Jul 2016

Position - Long

Premium - 0.7400 (quoted INR)

Although we know that the lot size is $1000 the quote does not mention it. This information is usually included in the quote for equity derivatives. If you're viewing this for the first-time, please be aware that the lot size of the equity derivatives is $1000.

What would the premium cost if you bought this option? This is easy to calculate.

Premium to be paid = Lot size * premium

= 1000 * 0.73400

=740

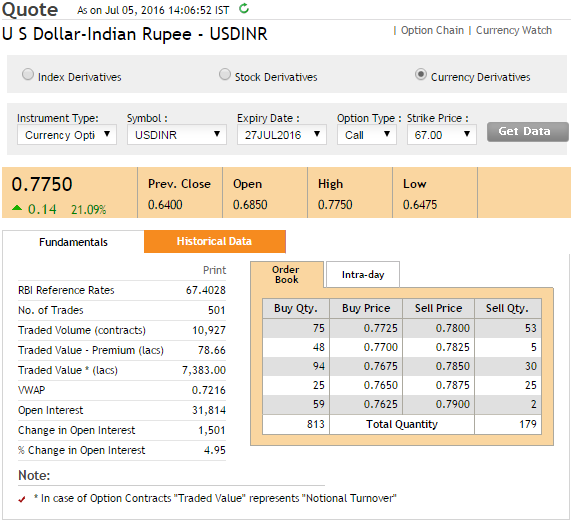

The option contract functions in the same way as equity derivative contracts. Another snapshot:

As you can see the premium has risen and I have the option to close my trade immediately. Here's how much I would make, if I did.

= 1000 * 0.77750

=775

This resulted in a profit of 775 to 740 = 35 per lot.

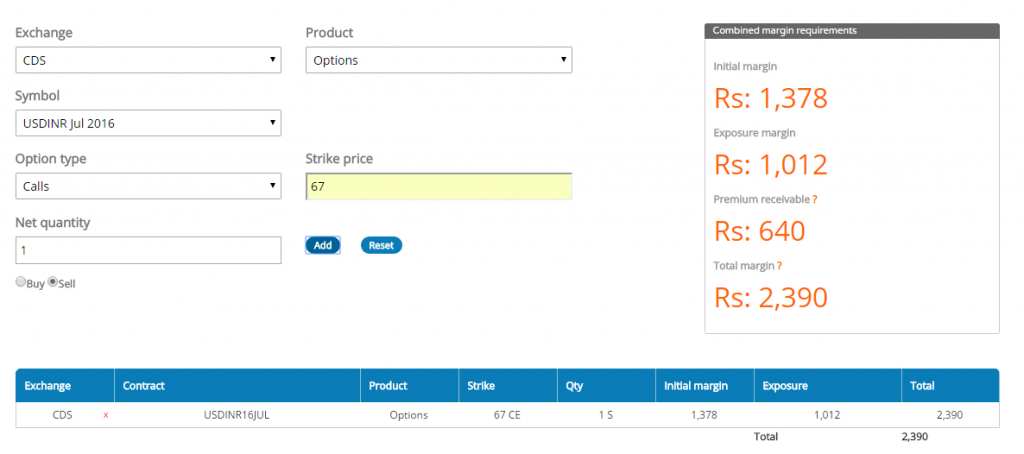

What if this option was to be sold/written instead? You already know that option selling involves you depositing margins.

Take a look at this snapshot. I used the calculator (shortening) to determine the required margin to write.

As you can see, there is a margin of Rs.2,390/.

This chapter should have given you an overview of the USD INR contract design. We will discuss the quantitative aspects of USD INR pairs and possibly look at contract specifications for other currencies in the next chapter.